Is 740 a good credit score? That's a question many people ponder when they receive their credit report. With a score of 740, you are sitting comfortably in the "good" range, but what does that mean for you? Understanding your credit score and how it affects your financial opportunities is crucial for making informed decisions. In this comprehensive guide, we will delve deep into what a 740 credit score signifies, how it stands in the broader credit score spectrum, and its potential impact on your financial life.

Credit scores play a pivotal role in our financial health. They can influence everything from loan approvals to the interest rates you're offered. A score of 740 is generally considered above average and can open doors to favorable lending terms. However, grasping the nuances of what constitutes a "good" credit score and how to maintain or improve it can be a game-changer in your financial journey.

Throughout this article, we'll explore the intricacies of credit scores, the benefits of having a 740 credit score, and offer actionable insights to help you maintain or even enhance your score. Whether you're a financial novice or a seasoned pro, understanding the significance of a 740 credit score will empower you to navigate the world of credit with confidence.

Table of Contents

- Understanding Credit Score Basics

- The Credit Score Range Explained

- The Significance of a 740 Credit Score

- Benefits of Having a 740 Credit Score

- Tips to Improve Your Credit Score Beyond 740

- Maintaining a Good Credit Score

- Loan Approvals and a 740 Credit Score

- Impact on Interest Rates

- Understanding Credit Utilization

- The Importance of Credit History

- The Role of Credit Mix

- Effects of New Credit Inquiries

- Debunking Credit Score Myths

- Future Trends in Credit Scoring

- Frequently Asked Questions

- Conclusion

Understanding Credit Score Basics

Credit scores are numerical representations of a person's creditworthiness. These scores are calculated based on the individual's credit history, which includes factors like payment history, amounts owed, length of credit history, types of credit in use, and new credit inquiries. The most commonly used credit scoring model is the FICO Score, which ranges from 300 to 850.

Each credit bureau—Experian, Equifax, and TransUnion—may have slightly different data, leading to variations in scores. However, the basic principles of scoring remain the same. A higher score indicates a lower risk to lenders, translating into better borrowing terms and conditions.

Understanding these basics is the first step in managing your credit effectively. Your credit score affects not only your ability to secure loans but also the interest rates you'll pay. It can also influence other areas of your life, such as renting a home or even job applications, where employers may consider credit scores as part of their vetting process.

The Credit Score Range Explained

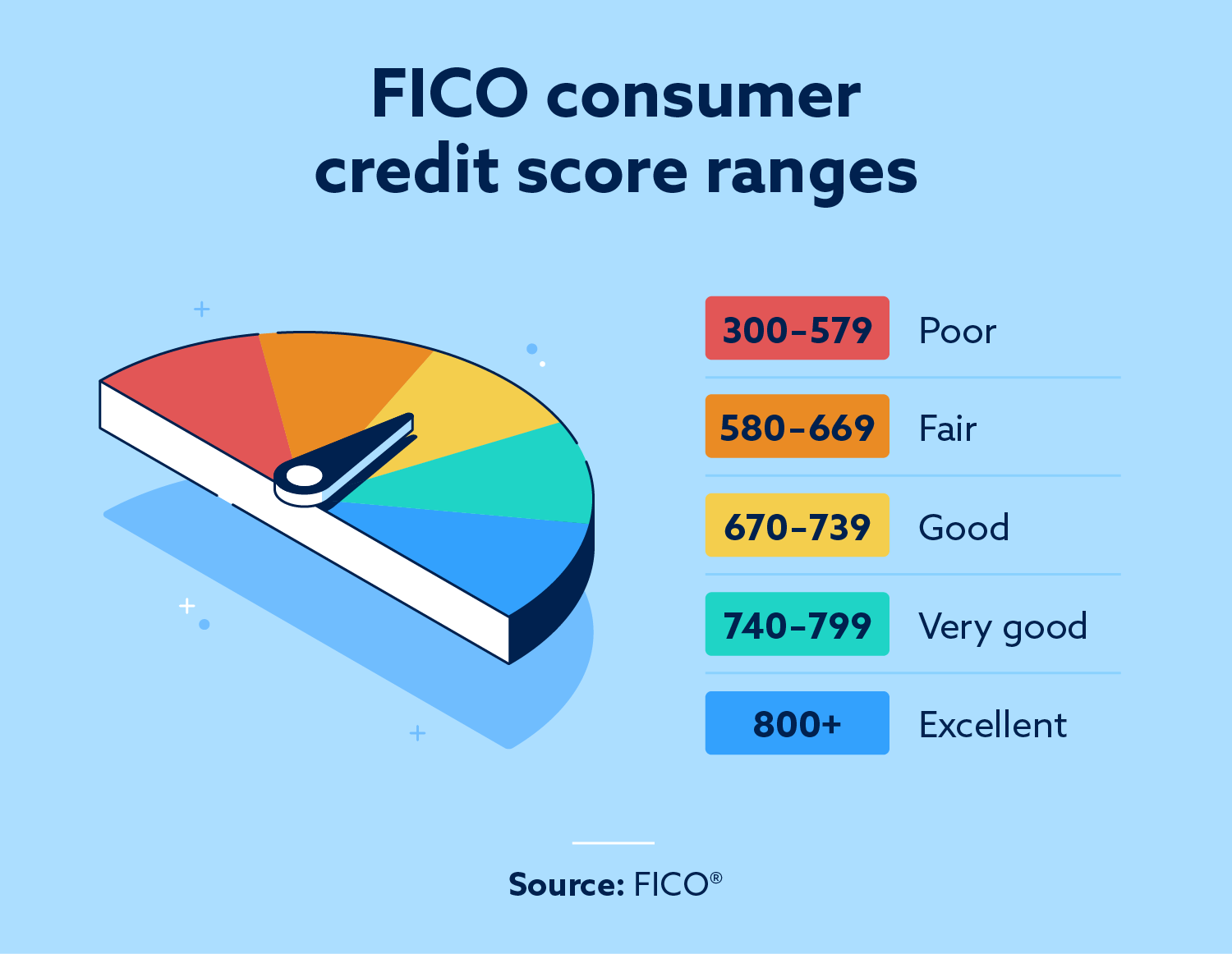

Credit scores typically fall within the following ranges:

- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Very Good

- 800-850: Exceptional

A score of 740 places you in the "Very Good" range, which means you're likely to qualify for attractive loan terms and interest rates. It's important to note that while a 740 is a commendable score, there's always room for improvement.

Being in the "Very Good" range signals to lenders that you are a responsible borrower who has a history of managing credit well. This can be beneficial when negotiating loan terms or seeking new credit opportunities. However, maintaining or improving your score requires consistent attention to your credit habits.

The Significance of a 740 Credit Score

Achieving a credit score of 740 is a noteworthy accomplishment that reflects responsible credit management. This score is a testament to your ability to manage debt and make timely payments. It's a significant step up from the "Good" range and offers more financial flexibility.

With a 740 credit score, you're likely to be viewed favorably by lenders, making it easier to secure loans, credit cards, and other financial products. This score can also lead to lower interest rates, which can save you money over time.

While a 740 is an excellent score, it's important to continue practicing good credit habits to maintain or even improve your score. This includes paying bills on time, keeping credit card balances low, and avoiding unnecessary credit inquiries.

Benefits of Having a 740 Credit Score

A 740 credit score comes with numerous benefits that can enhance your financial well-being. Here are some of the key advantages:

- Lower Interest Rates: With a 740 score, you're likely to qualify for lower interest rates on loans and credit cards, which can result in significant savings over time.

- Better Loan Terms: Lenders may offer more favorable loan terms, such as longer repayment periods or higher loan amounts, based on your credit score.

- Increased Approval Chances: A 740 score boosts your chances of being approved for loans, credit cards, and rental applications.

- Insurance Premiums: Some insurance companies use credit scores to determine premiums, so a higher score could lead to lower rates.

- More Credit Card Options: With a 740 score, you have access to a wider range of credit card options, including those with rewards and lower interest rates.

These benefits demonstrate the value of maintaining a healthy credit score and the positive impact it can have on your financial life.

Tips to Improve Your Credit Score Beyond 740

While a 740 credit score is impressive, there's always room for improvement. Here are some tips to help you boost your score even further:

- Pay Bills on Time: Consistently paying your bills on time is one of the most effective ways to improve your credit score.

- Reduce Credit Card Balances: Keeping your credit card balances low relative to your credit limit can positively impact your score.

- Avoid New Credit Inquiries: Limit the number of new credit inquiries, as too many can temporarily lower your score.

- Increase Credit Limits: Requesting a credit limit increase can improve your credit utilization ratio, which can boost your score.

- Monitor Your Credit Report: Regularly check your credit report for errors and dispute any inaccuracies that could affect your score.

By following these strategies, you can work towards achieving an even higher credit score, opening up more financial opportunities.

Maintaining a Good Credit Score

Once you've achieved a 740 credit score, maintaining it is crucial. Here are some tips to help you sustain a good credit score:

- Set Up Payment Reminders: Use payment reminders or automatic payments to ensure you never miss a due date.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit limit to maintain a healthy credit utilization ratio.

- Limit New Credit Applications: Avoid applying for new credit unless necessary to prevent unnecessary inquiries.

- Maintain a Diverse Credit Mix: A mix of credit types, such as credit cards, installment loans, and mortgages, can positively impact your score.

- Regularly Review Your Credit Report: Stay informed about your credit status by checking your credit report regularly.

By adhering to these practices, you can ensure your credit score remains strong, providing you with financial stability and opportunities.

Loan Approvals and a 740 Credit Score

With a 740 credit score, you are well-positioned to secure loan approvals for various financial needs. Whether you're applying for a mortgage, auto loan, or personal loan, your credit score plays a pivotal role in the lender's decision-making process.

Lenders view a 740 score as a sign of reliability, increasing your chances of approval for loans with favorable terms. This includes lower interest rates, reduced fees, and more flexible repayment options.

However, it's important to remember that other factors, such as your income, employment history, and debt-to-income ratio, also influence loan approvals. Maintaining a strong credit score in conjunction with a healthy financial profile can significantly enhance your borrowing power.

Impact on Interest Rates

A 740 credit score can have a substantial impact on the interest rates you're offered by lenders. Generally, higher credit scores translate into lower interest rates, which can save you a considerable amount of money over the life of a loan.

For example, with a 740 score, you may qualify for a mortgage with an interest rate that is 0.5% to 1% lower than someone with a lower credit score. This difference can result in thousands of dollars in savings over the term of a mortgage.

Similarly, credit cards and personal loans often come with more competitive rates for those with higher credit scores. This can make borrowing more affordable and help you manage your debt more effectively.

Understanding Credit Utilization

Credit utilization refers to the percentage of your available credit that you're currently using. It is a critical factor in credit scoring models, accounting for approximately 30% of your overall score.

To maintain a healthy credit utilization ratio, it's advisable to keep your credit card balances below 30% of your credit limit. For example, if you have a credit card with a $10,000 limit, aim to keep your balance below $3,000.

Lowering your credit utilization can have a positive impact on your credit score, as it indicates to lenders that you are managing your credit responsibly. Regularly monitoring and managing your credit utilization is an effective way to maintain or improve your credit score.

The Importance of Credit History

Your credit history is the record of your borrowing and repayment behavior over time. It includes information about your credit accounts, payment history, and any derogatory marks such as late payments or collections.

A longer credit history is generally seen as favorable, as it provides lenders with more information about your financial behavior. It demonstrates your ability to manage credit responsibly over time.

To build and maintain a strong credit history, it's important to keep older accounts open, pay bills on time, and avoid negative marks on your credit report. A positive credit history can significantly contribute to a higher credit score.

The Role of Credit Mix

Credit mix refers to the variety of credit types you have in your credit report, such as credit cards, mortgages, auto loans, and student loans. Having a diverse credit mix can positively impact your credit score, as it demonstrates your ability to manage different types of credit responsibly.

While it's not necessary to have every type of credit, a balanced mix can contribute to a stronger credit profile. For example, if you primarily have credit cards, adding an installment loan or a mortgage can enhance your credit mix.

However, it's important to only take on credit that you can manage effectively. Avoid opening new accounts solely to diversify your credit mix, as this can lead to unnecessary debt and potential financial strain.

Effects of New Credit Inquiries

When you apply for new credit, such as a loan or credit card, the lender typically performs a hard inquiry on your credit report. While a single inquiry may have a minimal impact on your score, multiple inquiries within a short period can lower your score.

It's important to be mindful of how often you apply for new credit. Limiting new credit applications can help protect your credit score from unnecessary dips.

If you're shopping for a loan, such as a mortgage or auto loan, try to complete your applications within a short time frame to minimize the impact of multiple inquiries. Credit scoring models often treat multiple inquiries for the same type of loan as a single inquiry if they're made within a certain period.

Debunking Credit Score Myths

There are many misconceptions about credit scores that can lead to confusion and potentially harm your financial health. Here are some common credit score myths debunked:

- Myth: Checking your own credit score lowers it. Fact: Checking your own credit score is considered a soft inquiry and does not affect your score.

- Myth: Closing unused credit cards improves your score. Fact: Closing credit cards can reduce your available credit and increase your credit utilization, potentially lowering your score.

- Myth: Paying off a debt removes it from your credit report. Fact: Paid debts remain on your credit report for up to seven years, but their impact diminishes over time.

- Myth: You have only one credit score. Fact: You have multiple credit scores based on different scoring models and credit bureau data.

- Myth: Income affects your credit score. Fact: Your income is not a factor in your credit score; however, it may be considered by lenders during the application process.

Understanding these myths can help you make more informed decisions about managing your credit and maintaining a healthy score.

Future Trends in Credit Scoring

The world of credit scoring is constantly evolving, with new trends and technologies shaping the way creditworthiness is assessed. Here are some emerging trends in credit scoring:

- Alternative Data: Lenders are increasingly looking at alternative data sources, such as utility payments and rental history, to assess creditworthiness.

- AI and Machine Learning: Advanced algorithms and machine learning are being used to develop more accurate and nuanced credit scoring models.

- Financial Inclusion: Efforts are being made to include underserved populations in the credit system, offering them more opportunities to build credit.

- Real-Time Updates: Credit scoring models are moving towards real-time updates, providing more current and dynamic assessments of creditworthiness.

- Greater Transparency: There is a push for more transparency in credit scoring, giving consumers better insight into how their scores are calculated.

Staying informed about these trends can help you adapt to changes in the credit landscape and maintain a strong credit profile.

Frequently Asked Questions

- What is considered a good credit score? A good credit score typically falls between 670 and 739, with a score of 740 considered very good.

- How can I improve my credit score quickly? Paying bills on time, reducing credit card balances, and avoiding new credit inquiries can help improve your score.

- Does checking my own credit score affect it? No, checking your own credit score is a soft inquiry and does not impact your score.

- How often should I check my credit report? It's advisable to check your credit report at least once a year to ensure accuracy and monitor for any signs of fraud.

- Can I get a mortgage with a 740 credit score? Yes, a 740 credit score is considered favorable for securing a mortgage with competitive terms.

- What factors affect my credit score? Key factors include payment history, credit utilization, length of credit history, credit mix, and new credit inquiries.

Conclusion

A 740 credit score is a strong indicator of financial responsibility and opens up numerous opportunities for favorable lending terms and financial products. Understanding the factors that contribute to your credit score and adopting good credit habits can help you maintain or improve your score over time.

By staying informed about credit scoring trends and debunking common myths, you can make better financial decisions and protect your credit health. Whether you're aiming to buy a home, secure a loan, or simply manage your finances more effectively, a good credit score is a valuable asset on your financial journey.